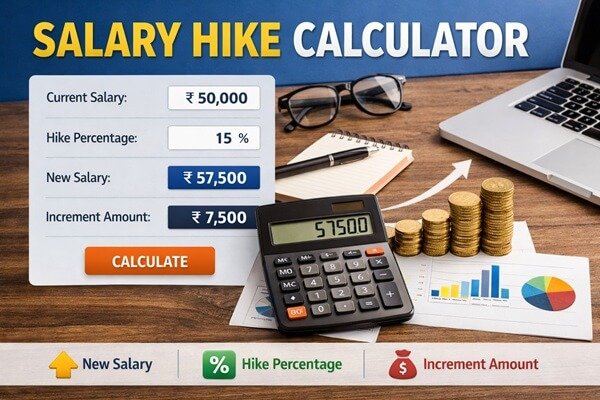

Salary Hike Calculator

Find your new salary, calculate the hike percentage, and compare multiple increment scenarios — all in one place.

📊 Salary Breakdown

📊 Salary Comparison

🔀 Multi-Scenario Hike Comparison

What Is a Salary Hike and Why Does It Matter?

Every year, millions of working professionals across India sit through their annual appraisal and walk out wondering — "Was that hike actually good?" A salary hike, also called a salary increment, is the percentage increase applied to your current pay. It sounds simple, but the implications go far beyond a single number. It affects your take-home pay, your tax bracket, your EPF contribution, and — if you're thinking about switching jobs — your negotiating power for the next offer.

A 10% hike on ₹40,000 adds ₹4,000 a month. The same 10% on ₹1,20,000 adds ₹12,000. The percentage is the same, the rupee difference is worlds apart. That's why having a clear, reliable calculator matters — so you know exactly where you stand, not just roughly.

How to Calculate Salary Hike — The Formula

There are two directions you might want to calculate a hike, and both are covered in the calculator above.

Formula 1: Find Your New Salary from Hike %

New Salary = Current Salary × (1 + Hike% ÷ 100)

Example: Current salary = ₹60,000/month, Hike = 12%

New Salary = ₹60,000 × 1.12 = ₹67,200/month

Monthly increment = ₹7,200 | Annual increment = ₹86,400

Formula 2: Find Hike % from Two Salaries

Hike % = ((New Salary − Current Salary) ÷ Current Salary) × 100

Example: Current salary = ₹50,000, New offer = ₹65,000

Hike % = ((65,000 − 50,000) ÷ 50,000) × 100 = 30%

This second formula is particularly useful when you receive a job offer and want to know how good it actually is compared to what you're earning today.

What Is a "Good" Salary Hike in India? (2025 Benchmarks)

This is the question everyone really wants answered. Here's a realistic picture of how salary increments work across different situations in India:

| Scenario | Typical Hike Range | What It Signals |

|---|---|---|

| Annual appraisal (average performer) | 5–8% | Standard cost-of-living raise |

| Annual appraisal (good performer) | 8–12% | Performance recognised |

| Annual appraisal (top performer) | 12–20% | Strong contribution, retention priority |

| Internal promotion | 15–30% | Role change with more responsibility |

| Job switch (same domain) | 20–40% | Market rate adjustment |

| Job switch (new domain/city) | 30–60% | Skill premium + location adjustment |

| Counter-offer from current employer | 15–25% | Retention bid |

According to industry surveys for FY 2025–26, the average salary hike in India across sectors is expected to be around 9–10%, with IT/tech, pharma, and BFSI typically offering higher increments than manufacturing and retail. These are averages — individual outcomes depend heavily on performance ratings, team budgets, and how well you negotiate.

Salary Hike vs CTC Hike — Not Always the Same Thing

Here's something that catches a lot of people off guard. A "20% hike in CTC" doesn't necessarily mean a 20% increase in your monthly take-home. Why? Because your CTC (Cost to Company) includes components like employer EPF contribution, gratuity provisions, and variable pay — none of which land in your bank account monthly.

So if your new CTC is inflated by a higher variable bonus component or a bigger employer PF contribution, your fixed monthly pay might increase by much less than the headline hike percentage suggests.

Always ask for — and compare — the fixed monthly salary and the take-home / net salary when evaluating a new offer. The CTC number alone can be misleading.

Industry-Wise Average Salary Hike in India (2025–26)

| Industry | Average Hike (Appraisal) | Job Switch Hike |

|---|---|---|

| IT / Software | 8–12% | 25–50% |

| BFSI (Banking, Finance, Insurance) | 8–11% | 20–40% |

| Pharma / Healthcare | 9–13% | 20–35% |

| E-commerce / Startups | 10–15% | 25–60% |

| Manufacturing | 6–9% | 15–25% |

| FMCG / Retail | 7–10% | 15–30% |

| Consulting | 9–14% | 20–40% |

| Education | 5–8% | 10–20% |

How to Use the Multi-Scenario Comparison

The scenario comparison section above is something you won't find on most hike calculators. It lets you enter your current salary once, and instantly see what your new salary would look like at five different hike percentages simultaneously — from a modest 5% to a healthy 30%.

This is incredibly useful in two situations:

- Before your appraisal: You can set realistic expectations and know what number to walk in asking for.

- When evaluating a job offer: If you're weighing two offers with different hike percentages, seeing them side by side makes the decision easier.

The "BEST" label highlights the highest hike scenario so the best option is always visually obvious at a glance.

How a Salary Hike Affects Your Taxes and Take-Home Pay

A salary hike doesn't all go into your pocket. Here's what changes when your salary increases:

Income Tax

If your salary crosses a tax slab boundary after the hike, a portion of your increment will be taxed at a higher rate. Under the new tax regime for FY 2025–26, the slabs are fairly broad (0%, 5%, 10%, 15%, 20%, 25%, 30%), so not every hike triggers a bracket jump — but it's worth checking. For example, if your taxable income moves from ₹11.9L to ₹12.5L, you'd start paying 15% on that ₹60,000 instead of 10%.

EPF (Employee Provident Fund)

Your EPF contribution is 12% of your basic salary. If your basic pay increases with the hike, your EPF deduction increases too — which reduces take-home in the short term but builds your retirement corpus faster. On the positive side, your employer's EPF contribution also increases.

Professional Tax

In some states, professional tax is deducted at a fixed slab. Crossing a threshold (say, ₹25,000/month in Maharashtra) may slightly increase this deduction, though the amounts are small (typically ₹200–300/month max).

The Net Effect

As a rough rule of thumb: for every ₹100 of gross salary hike, expect ₹65–80 to reach your bank account as net take-home, depending on your tax bracket and EPF structure. The rest goes to deductions. This is why the "hike percentage" you celebrate on appraisal day and the "extra money in your account" feel slightly different.

Salary Negotiation — How to Ask for More

Having the numbers is just the start. Here's how to turn them into a successful negotiation:

- Know the market rate first. Use salary data from LinkedIn, Glassdoor, AmbitionBox, or industry surveys. If the market pays 20% more than what you're earning, you have a strong case.

- Quantify your contributions. Vague claims like "I worked hard" don't move the needle. Specific numbers do: "I led a project that increased revenue by ₹15L" or "reduced processing time by 30%".

- Don't anchor low. When asked for your expected hike, name a number 5–8% higher than what you'd actually accept. This gives room to negotiate down and still land where you want.

- Compare total compensation, not just base. Bonuses, stock options, flexible work, extra leave — these have real monetary value and should be part of any comparison.

- Time it right. The best time to negotiate is after a visible win, not in the middle of a tough quarter. Annual reviews are obvious, but project completions and promotions are also great moments.

Salary Hike Quick Reference Table

| Current Monthly Salary | 10% Hike | 15% Hike | 20% Hike | 30% Hike |

|---|---|---|---|---|

| ₹20,000 | ₹22,000 | ₹23,000 | ₹24,000 | ₹26,000 |

| ₹40,000 | ₹44,000 | ₹46,000 | ₹48,000 | ₹52,000 |

| ₹60,000 | ₹66,000 | ₹69,000 | ₹72,000 | ₹78,000 |

| ₹80,000 | ₹88,000 | ₹92,000 | ₹96,000 | ₹1,04,000 |

| ₹1,00,000 | ₹1,10,000 | ₹1,15,000 | ₹1,20,000 | ₹1,30,000 |

| ₹1,50,000 | ₹1,65,000 | ₹1,72,500 | ₹1,80,000 | ₹1,95,000 |

Frequently Asked Questions

Note: All calculations are estimates based on gross salary. Actual take-home pay will vary based on your tax regime, salary structure, EPF contributions, and other deductions. Consult your HR or a financial advisor for exact figures.